India’s electric vehicle (EV) industry is rapidly expanding, and a new report suggests the country is well-positioned to become a global manufacturing hub for EV components. According to a joint study by the Institute for Energy Economics and Financial Analysis (IEEFA) and JMK Research & Analytics, India targets 90-100 % EV component localisation across several non-battery categories by 2030. However, the report also warns that heavy dependence on imported semiconductors, rare-earth magnets, and battery cells could limit true domestic value creation.

India Targets 90-100 % EV Component Localisation by 2030

The report states that India targets 90-100 % EV component localisation across several non-battery categories by the end of the decade. India’s EV market has witnessed remarkable growth, with sales increasing nearly 14 times since FY2020, creating enormous opportunities for domestic manufacturing.

Strong investments in powertrains, electric motors, power electronics, vehicle control units, charging infrastructure, and thermal management systems are expected to help the country reach near-complete localisation in these segments by 2030.

However, researchers note that localisation should not be measured only by final assembly. A significant portion of the core technologies and raw materials used in these components still comes from overseas suppliers.

India Has Strong Manufacturing Capabilities in Traditional Auto Components

The report highlights that India has already built a strong manufacturing base in several conventional automotive components. These include:

- Structural components

- Suspension systems

- Braking systems

- Wiring harnesses

These established manufacturing strengths provide a solid foundation for expanding into high-value EV-specific components.

As India targets 90-100 % EV component localisation, these existing capabilities are expected to support faster growth across the electric mobility supply chain.

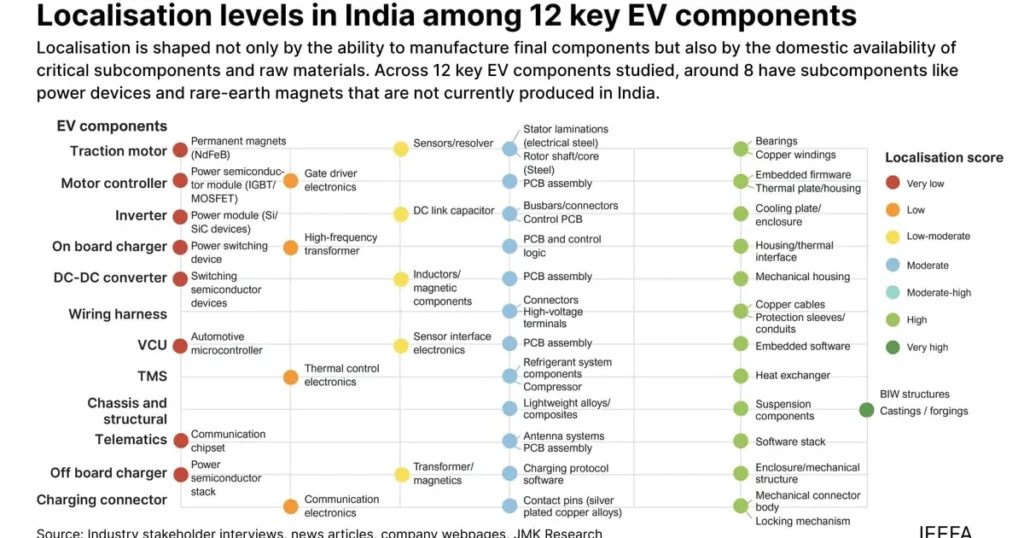

Semiconductors and Rare-Earth Magnets Remain the Biggest Challenges

Despite the encouraging localisation outlook, the report identifies several critical bottlenecks that continue to slow India’s journey toward complete manufacturing independence.

Among the biggest concerns are the following:

- Heavy dependence on imported semiconductors used in vehicle control units and power electronics.

- Rare-earth magnets are required for high-efficiency electric motors, with global processing dominated by China.

- Continued imports of lithium-ion battery cells, even though battery pack assembly increasingly takes place within India.

Researchers warn that these upstream dependencies expose India’s EV industry to geopolitical risks, supply disruptions, and price volatility.

PLI Scheme Driving Investments, but Fund Disbursement Remains Slow

The report also evaluates the government’s Production-Linked Incentive (PLI) Scheme for Automobile and Auto Components, which has played an important role in encouraging domestic manufacturing.

Around 60% of recent non-battery EV component manufacturing announcements have come from companies approved under the scheme.

Although the government allocated ₹25,938 crore under the programme, less than 10% of the available funds had been disbursed by early 2026.

According to the report, strict domestic value addition (DVA) requirements and complex compliance procedures have slowed the release of financial incentives to manufacturers.

Experts Recommend Four Key Steps for Deeper Localisation

The study emphasizes that achieving meaningful localisation requires more than assembling imported components. Experts recommend several strategic measures to strengthen India’s EV supply chain:

- Develop domestic semiconductor manufacturing facilities.

- Build rare-earth processing and magnet production capabilities.

- Promote component standardisation to improve supplier scale and reduce manufacturing costs.

- Expand participation of EV startups in localization programs.

- Increase investment in indigenous research and development to reduce reliance on imported technologies and advanced materials.

These initiatives would help India move beyond assembly-led manufacturing and create higher domestic value across the EV ecosystem.

Outlook for India’s EV Manufacturing Sector

The report concludes that India targets 90-100 % EV component localisation in several manufacturing segments by 2030, but success will depend on strengthening upstream technologies and reducing reliance on imported critical materials.

While India’s traditional automotive manufacturing expertise and expanding EV investments provide a strong foundation, developing domestic capabilities in semiconductors, rare-earth magnets, advanced materials, and battery technologies will be essential for long-term competitiveness.

If these challenges are addressed through policy support, investment, innovation, and stronger supply chains, India targets that 90-100 % EV component localisation could become a significant milestone in establishing the country as a global electric vehicle manufacturing hub.

Related Articles: